Accrual Accounting

Understanding Accrual Accounting

Alright, let’s sit down and have a proper chat about accrual accounting. Imagine we’re in a cosy Irish café, with a pot of tea and some freshly baked scones, delving into this concept that’s a bit more involved than just tracking cash in and out of your business.

The Theory of Accrual Accounting

At its core, accrual accounting is about capturing the financial effects of business actions and events as they happen, not just when the money changes hands. It’s a comprehensive method that provides a fuller picture of your business’s financial health by recognising revenues and expenses in the periods they occur, rather than when the cash is received or paid.

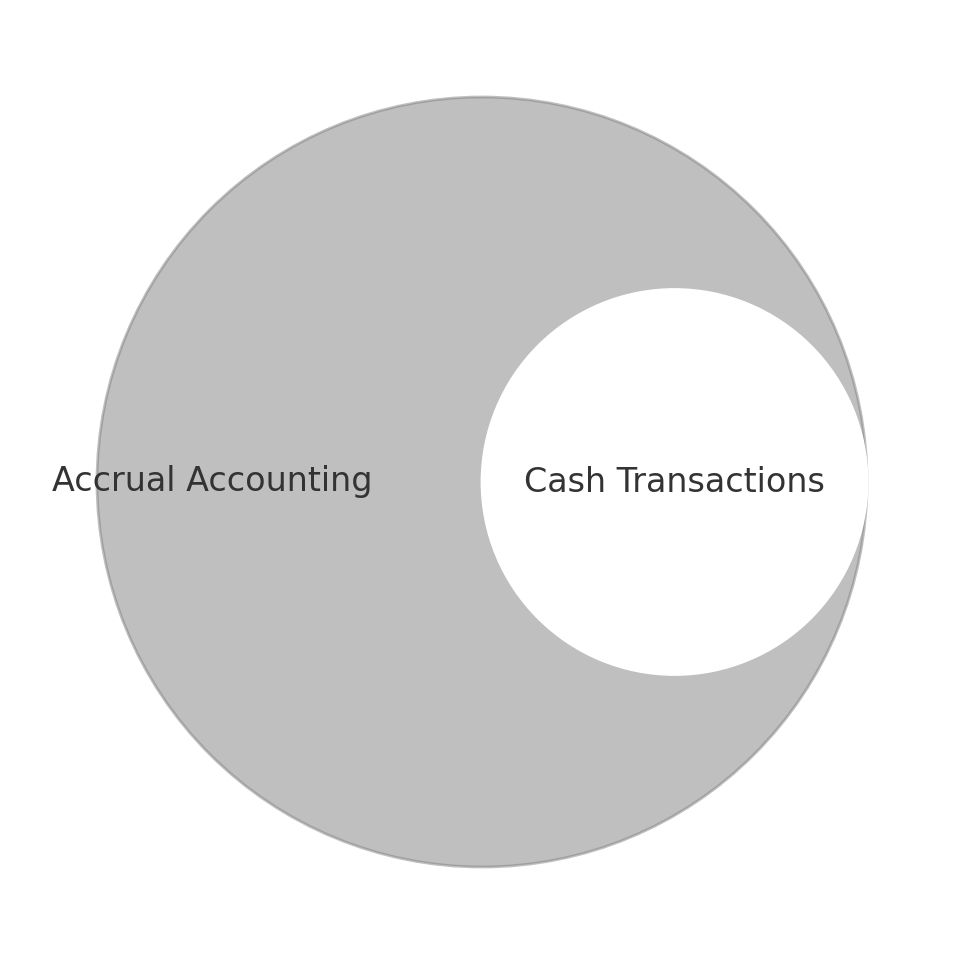

To get a better grasp of this, think of two circles. The smaller circle represents cash transactions – simple, straightforward, and focused solely on when cash enters or leaves your account. The larger circle represents accrual accounting, encompassing everything within the smaller circle but also covering a whole lot more. This larger circle includes all actions and events measured in terms of money over time.

The Axis of Time and Money

In accrual accounting, we plot financial actions and events along two axes: time and money. This means that any business activity that has a financial impact is recorded at the moment it occurs, based on its monetary value, even if the actual cash movement happens later.

This means the student of accounting must now become acutely aware of various real-world events and actions that influence the financial statements. The physical movement of goods, the intangible effort of employees working, the passage of time, and the provision of intangible services all come into new focus.

Receiving Stock

Let’s say you run a quaint little bookshop. On the 1st of April, you receive a delivery of new books worth €1,000, but you’re not due to pay the supplier until the 15th of April.

Cash Transactions

In cash accounting, you’d only record this transaction on the 15th of April when you actually hand over the €1,000.

Accrual Accounting

With accrual accounting, on the 1st of April, you would record the books as inventory (an asset) worth €1,000.

Simultaneously, you’d record a liability of €1,000 under accounts payable, as you owe this amount to the supplier.

When you pay the supplier on the 15th of April, you would then reduce your cash by €1,000 and decrease your accounts payable by €1,000.

Journal Entries

April 1st

- Debit: Inventory €1,000

- Credit: Accounts Payable €1,000

April 15th

- Debit: Accounts Payable €1,000

- Credit: Cash €1,000

This way, accrual accounting captures the moment you receive the inventory and recognise the obligation to pay, providing a more accurate picture of your financial position as of the 1st of April.

Electricity Usage

Your bookshop uses electricity every day to keep the lights on and the registers running. Let’s say your monthly electricity bill is €300, which you receive and pay on the 5th of the following month.

Cash Transactions

- In cash accounting, you’d record the €300 expense only on the 5th of the next month when you pay the bill.

Accrual Accounting

- In accrual accounting, you’d spread this cost over each day of the month, recognising that you use electricity daily.

- By the end of the month, you’d have recorded a total expense of €300 for electricity used.

Journal Entries

Daily (simplified as monthly)

- Debit: Electricity Expense €300

- Credit: Accrued Expenses (or Accounts Payable) €300

Following Month (when you pay the bill)

- Debit: Accrued Expenses (or Accounts Payable) €300

- Credit: Cash €300

Here, accrual accounting matches the electricity expense to the period it was incurred, reflecting the actual usage and cost more accurately within the month.

Employee Wages

Your employees work every day, but you pay them at the end of the month. Let’s say your total payroll for April is €5,000.

Cash Transactions

- In cash accounting, you’d record the €5,000 expense at the end of April when you pay your employees.

Accrual Accounting

- With accrual accounting, each day, you accrue a portion of the payroll expense, acknowledging that your employees earn their wages daily.

- By the end of April, you’d record a total payroll expense of €5,000.

Journal Entries

Daily (simplified as monthly)

- Debit: Wages Expense €5,000

- Credit: Wages Payable €5,000

End of Month (when you pay the employees)

- Debit: Wages Payable €5,000

- Credit: Cash €5,000

Accrual accounting ensures that wages are recorded in the period employees work, reflecting the true cost of labour throughout the month.

Sales on Credit

Let’s say on the 10th of May, you sell €2,000 worth of books to a customer on credit, and they will pay you at the end of May.

Cash Transactions

- In cash accounting, you’d only record this sale when the payment is received at the end of May.

Accrual Accounting

- On the 10th of May, you would record the revenue of €2,000, because you’ve earned it by providing the books.

- You’d also record an accounts receivable (an asset) of €2,000.

Journal Entries

May 10th

- Debit: Accounts Receivable €2,000

- Credit: Sales Revenue €2,000

End of May (when you receive the payment)

- Debit: Cash €2,000

- Credit: Accounts Receivable €2,000

This approach recognises the revenue when the sale is made, reflecting your earned income immediately rather than waiting for the cash to arrive.

Sales for Cash

Let’s look at a straightforward cash sale. On the 15th of June, a customer buys €500 worth of books and pays in cash.

Cash Transactions

- You’d record the sale and cash receipt immediately on the 15th of June.

Accrual Accounting

- The same approach applies since the cash and sale occur simultaneously.

Journal Entries

June 15th

- Debit: Cash €500

- Credit: Sales Revenue €500

In this case, both methods align because the transaction is instant.

Why Accrual Accounting Matters

Accrual accounting is essential because it provides a comprehensive view of your business’s financial health. It adheres to the matching principle, which means expenses are recorded in the same period as the revenues they help generate. This principle ensures that you see the true profitability of your business activities.

The Student’s New Perspective

For the student of accounting, understanding accrual accounting means gaining a deeper awareness of the real-world events and activities that drive financial outcomes. The physical movement of goods, like receiving inventory, becomes crucial. The daily work of employees is recognised as a continuous expense, not just when they’re paid. The passage of time takes on new significance as it affects when expenses are incurred and revenues are earned.

Even intangible services, like a doctor examining a patient or someone using transportation, must be accounted for when they occur, not just when the payment is made. These actions and events, once perhaps taken for granted, now come into sharp focus as the student learns to map them accurately in the financial records.

Key Benefits of Accrual Accounting

Accuracy

By recording revenues and expenses when they occur, accrual accounting presents a more accurate financial picture.

Compliance

Many accounting standards and regulations require accrual accounting, especially for larger businesses.

Planning and Decision-Making

With a clearer view of your finances, you can make better-informed decisions and plan more effectively for the future.

Financial Health

Understanding your true financial position helps in managing cash flow, securing financing, and evaluating business performance.

Visualising the Concept

To visualise accrual accounting, think of two circles. The smaller circle represents cash transactions, simple and straightforward. The larger circle represents accrual accounting, which includes the smaller circle but also covers a broader range of activities and their financial impacts over time.

Inside the Larger Circle

- Stock Delivery : Recognising inventory and liability when received, not just when paid.

- Electricity Usage : Accruing daily expenses rather than recording them only when the bill is paid.

- Employee Wages : Accruing wages as they are earned, not just when paid.

- Credit Sales : Recognising revenue when earned, not just when cash is received.

- Cash Sales : Recording sales and cash receipts simultaneously.

A Day in the Life of a Business Using Accrual Accounting

Let’s take a day in the life of our bookshop to see how accrual accounting captures everything.

Morning

- Stock Delivery : Fresh books arrive, worth €500. These are recorded as inventory with a corresponding liability to the supplier.

- Entry : Debit Inventory €500, Credit Accounts Payable €500.

Midday

- Sales on Credit : A corporate client orders books worth €1,000 on credit. This is recorded as revenue and an asset (accounts receivable).

- Entry : Debit Accounts Receivable €1,000, Credit Sales Revenue €1,000.

Afternoon

- Cash Sales : Walk-in customers buy books for €200 cash. This is recorded as revenue and cash.

- Entry : Debit Cash €200, Credit Sales Revenue €200.

- Electricity Usage : Electricity is used throughout the day. Let’s assume the daily cost is €10.

- Entry : Debit Electricity Expense €10, Credit Accrued Expenses €10.

Evening

- Employee Wages : Employees work and earn wages. The daily wage cost is €250.

- Entry : Debit Wages Expense €250, Credit Wages Payable €250.

End of the Month

At the end of the month, you pay your bills and wages:

- Paying SupplierYou pay the supplier for the books.

- Entry : Debit Wages Expense €250, Credit Wages Payable €250.

- Receiving Payment from Client : The corporate client pays their bill.

- Entry : Debit Cash €1,000, Credit Accounts Receivable €1,000.

- Paying Electricity Bill : You pay the electricity bill for the month.

- Entry : Debit Accrued Expenses €300, Credit Cash €300.

- Paying Wages : You pay your employees their monthly wages.

- Entry : Debit Wages Payable €7,500, Credit Cash €7,500.

Wrapping Up

Accrual accounting paints a fuller picture of your business’s financial health by capturing all the actions, events, and physical items measured in terms of money over time. It includes, but is not limited to, cash transactions. By understanding and using accrual accounting, you’re better equipped to see how your business is really doing, making it easier to plan and make informed decisions.

So, while it might seem a bit more involved than just tracking cash, it’s well worth the effort. You’ll have a clearer view of your financial landscape, making it as detailed and accurate as a well-crafted tapestry. And as a student of accounting, you’ll gain a newfound appreciation for how every action, whether it’s the movement of goods, the work of employees, or the provision of services, fits into the broader financial picture.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo. Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

About Us

Legal

Location

Lorem ipsum dolor sit amet, consectetur adipiscing elit.

info@accounting-training.com

123-4567-890

Copyright ©2024 Accounting Training. All Rights Reserved

Course Outline

- Concepts and Accounting

- The Three Different Natures of Accounts

- The Accounting Equation

- Accrual Accounting

- Debits and Credits

- The Journal

- Bank Reconciliation

- Adjusting Entries

- Inventory and Cost of Sales

- Depreciation

- Income Statement

- Balance Sheet

- Chart of Accounts

- Accounting Principles

- Financial Accounting

- Financial Statements

- Working Capital and Liquidity

- Cash Flow Statement

- Financial Ratios

- Accounts Receivable and Bad Debts Expense

- Accounts Payable

- Inventory and Cost of Goods Sold

- Payroll Accounting

- Bonds Payable

- Stockholders’ Equity

- Present Value of a Single Amount

- Present Value of an Ordinary Annuity

- Future Value of a Single Amount

- Nonprofit Accounting

- Break-even Point

- Improving Profits

- Evaluating Business Investments

- Manufacturing Overhead

- Nonmanufacturing Overhead

- Activity Based Costing

- Standard Costing

- About WordPress

- Log In

- Register

- Elementor Debugger

- Page Template

- Theme

- Template File: WP Page Template > Elementor - header-footer.php

- Location: Header > Added By Condition > Header

- Location: Footer > Added By Condition > Footer

- Location: Popup > Added Manually > Course Outline Menu