Debits and Credits

Debits and credits are often a source of confusion for students learning accounting, partly due to the everyday meanings of these words in the English language. In non-accounting contexts, “debit” and “credit” are used with multiple meanings, many of which carry positive or negative connotations. For example, people often associate “credit” with something good, such as gaining or receiving something, while “debit” might be seen as something bad, like a deduction or expense. However, these interpretations can be misleading when it comes to understanding debits and credits in the context of accounting.

To overcome this confusion, it’s better to approach debits and credits not as good or bad but rather as a neutral, interlocking mathematical system designed to keep the accounting equation in balance. This system, which was invented in Europe before the acceptance of negative numbers, serves as the foundation for modern financial record-keeping and reporting. At its core, the accounting meaning of debits and credits is mathematical, and understanding them in this way can help students grasp the logic behind the system without the distractions of everyday language associations.

The Misleading Nature of Everyday Language

The first barrier to understanding debits and credits comes from the common uses of these terms in everyday language. For instance, when someone “debits” their bank account, it’s usually seen as withdrawing money or making a payment, which feels like a loss. Conversely, when someone “credits” their account, it’s typically interpreted as receiving money or gaining value, which feels positive. This conventional thinking leads students to believe that debits are inherently bad (because they “take away”) and credits are inherently good (because they “add”).

In accounting, however, debits and credits have no intrinsic positive or negative value. They are simply ways of categorizing and recording transactions to maintain the integrity of the accounting equation, which states:

Assets = Liabilities + Equity

Debits and credits are tools that ensure this equation is always in balance—what goes out from one account must come into another. The terms themselves derive from the Latin words “debere” (to owe) and “credere” (to believe or entrust), but in accounting, they don’t carry moral or emotional weight. Instead, debits and credits are technical terms indicating which side of an account a transaction affects. A debit simply means an entry on the left side of an account, while a credit refers to an entry on the right side.

A Mathematical System, Not Moral Judgments

When students are able to shed the associations of debits and credits with good and bad, they can begin to see these entries as part of an interconnected mathematical system. Each transaction in accounting affects at least two accounts: one that is debited and one that is credited. This concept is crucial to understanding how debits and credits work to maintain balance in the accounting equation.

For example, if a business buys equipment for cash, the transaction will increase one asset account (equipment) and decrease another asset account (cash). The equipment account would be debited (because it’s increasing in value), and the cash account would be credited (because it’s decreasing). The equation still balances because the total value of the assets hasn’t changed—only their composition has. In this case, the debit and credit entries reflect different sides of the same transaction without implying anything “good” or “bad” about it.

This mathematical balance is what makes double-entry accounting so powerful. It ensures that the books are always in equilibrium, and it allows accountants to trace the flow of transactions through various accounts, providing an accurate and complete picture of a company’s financial health.

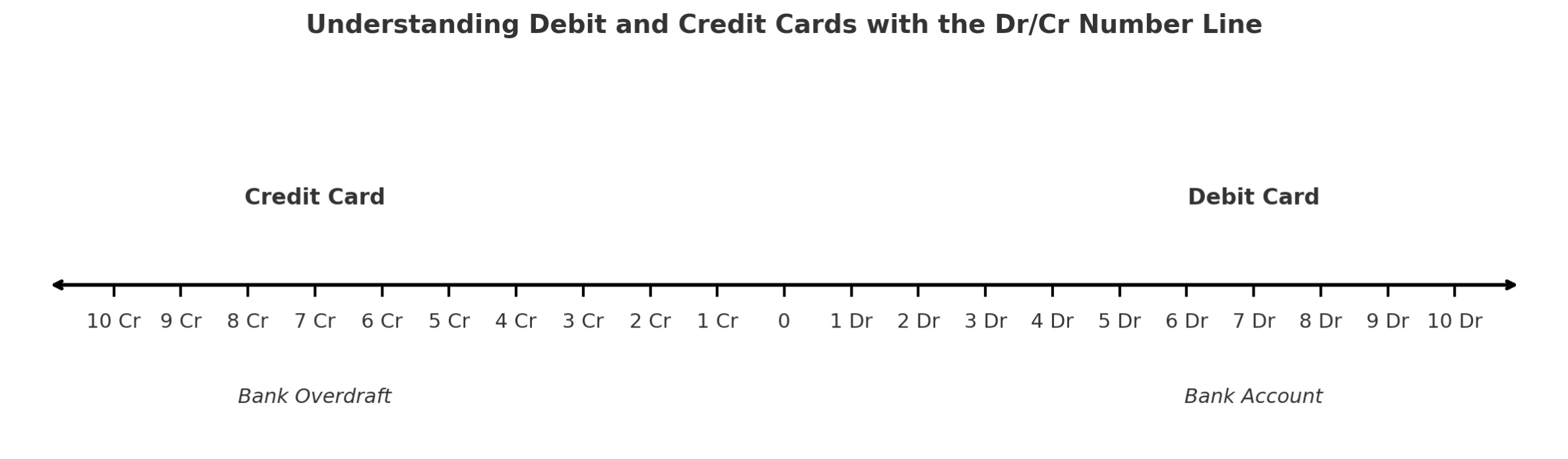

Debits and Credits as a Number Line

A useful way to conceptualize debits and credits is to think of them as functioning like pluses and minuses on a number line. Just as adding a positive number moves a point to the right and subtracting a number moves it to the left, debits and credits in accounting function in a similar way.

Understanding Debits and Credits Using the Number Line

A Quick Recap of History

Before negative numbers were widely accepted in European mathematics, accountants still needed a reliable way to represent both gains and losses in financial records. Although concepts similar to negative numbers had long been in use in other parts of the world, such as in Chinese and Indian mathematics, European scholars remained sceptical of their legitimacy well into the Renaissance. This scepticism created a practical challenge: how could you show a decrease in value or a debt without using a negative number?

The solution emerged in the form of the double-entry bookkeeping system—a method that allowed financial increases and decreases to be tracked through the balanced interplay of debits and credits. This system wasn’t invented by Luca Pacioli, but he was the first to formally document and publish it in a systematic way. His 1494 treatise, Summa de Arithmetica, Geometria, Proportioni et Proportionalità, included a section on bookkeeping that became the foundation for modern accounting practice.

This historical context helps explain why debits and credits might seem unintuitive to modern students who are accustomed to the clean algebra of positive and negative numbers. Yet if we approach the double-entry system not as a numerical puzzle but as a directional framework—one that balances movement between accounts rather than signs on a number line—it starts to make a lot more sense.

The Number Line: A Universal Tool

Let’s begin with something simple and familiar: the number line.

A number line is a straight, horizontal line with zero at the centre, positive numbers increasing to the right, and negative numbers decreasing to the left.

Moving to the right means you are adding a positive number.

Moving to the left means you are adding a negative number (which is the same as subtracting).

This directional model helps us visualize how numbers change.

An increase in value moves the position to the right.

A decrease in value moves it to the left.

It’s a straightforward way to understand how addition affects position—and it lays the foundation for thinking about direction and balance in more complex systems

Applying the Number Line to Debits and Credits

Let’s now apply the structure of the number line to the world of accounting.

Imagine a number line with zero at the centre, and let’s label the two sides:

- The right side is marked Dr (Debit)

- The left side is marked Cr (Credit)

It’s important to understand that this labelling is a convention, not a mathematical rule. We could just as easily reverse it—putting credits on the right and debits on the left. The system would still work because debits and credits are not inherently positive or negative. They’re directions of movement within a structured system.

So why mirror the mathematical number line, with debits on the right and credits on the left?

Because it helps us align accounting logic with mathematical intuition. In mathematics:

- Adding a positive number moves you to the right (Increase in an asset).

- Adding a negative number moves you to the left (a decrease or a liability).

When applied to accounting:

- Assets—such as cash, equipment, and inventory—are increased by debits. Placing debits on the right side mirrors the way we think of positive movement in maths.

- Liabilities and equity—which represent claims on those assets—are increased by credits. Placing credits on the left reflects the idea that these are obligations or interests that offset assets.

So, while the Dr/Cr structure isn’t fixed by mathematics, aligning it with the number line gives us a logical, visual way to understand how values shift—and how different types of accounts behave. It transforms the system from a set of memorized rules into something conceptually grounded and intuitive.

Visualizing Movement

To understand how debits and credits function as directional tools, it helps to visualize how values move along the number line.

Let’s break it down into two key types of movement:

Credit Movement (Leftward)

When you credit an account, imagine a movement to the left on the number line.

-

Credit an asset account → the value decreases

(You're moving toward zero or further into the Cr side.)

-

Credit a liability account → the value increases

(You're moving deeper into the Cr side—reflecting a greater obligation.)

In both cases, the credit shifts the balance leftward, but its effect depends on the type of account.

Debit Movement (Rightward)

When you debit an account, you’re moving to the right on the number line.

-

Debit an asset account → the value increases

(You’re moving further into the Dr side—gaining more of the asset.)

-

Debit a liability account → the value decreases

(You’re moving back toward zero—reducing what’s owed.)

Here again, the direction is the same—rightward—but the outcome depends on the nature of the account.

This visualization helps replace the idea of debits and credits being “positive” or “negative” with something more intuitive: movement and balance across a structured system.

Why This Matters

One of the most persistent challenges in learning accounting is that people come to the terms debit and credit with everyday associations—like “debit card” or “credit score”—rather than with any real mathematical framework. As a result, these terms often feel arbitrary or even contradictory.

But when we reconnect debits and credits to directional movement—using the number line as a visual tool—it all starts to make sense.

-

We see why increasing an expense is recorded as a debit:

Expenses reduce equity. Since equity increases on the credit (left) side of the number line, a rise in expenses pushes us in the opposite direction—rightward, which is a debit. -

We understand why decreasing revenue is also a debit:

Revenue increases equity (again, on the credit side), so reducing revenue means moving right—again, a debit. -

We clarify why liabilities increase with credits and assets increase with debits:

Liabilities and equity accounts grow on the left (Cr) side, while assets increase on the right (Dr). So increases push further in their respective directions—left for credits, right for debits.

The number line model gives us a way to stop relying on memorized rules and start seeing how the system actually works. It’s not about “Good” and “Bad” numbers—it’s about movement, direction, and balance. Once we view accounting in this light, the structure of double-entry bookkeeping becomes intuitive—just as it was originally intended.

Asset Account

For an asset account, a debit increases the value of the account, much like adding a positive number on a number line shifts the value further to the right. Conversely, a credit decreases the asset account value, moving it left on the number line, closer to zero or into negative territory.

For instance, imagine a company has an asset account—cash—with a debit balance of $10,000. If the company receives an additional $2,000 in cash, the account is debited, increasing the balance to $12,000. This is similar to moving further to the right on a number line, just as adding a positive number increases the value.

Asset Account

Now, suppose the company spends $3,000. This transaction is recorded as a credit to the cash account, decreasing the balance to $7,000. This credit acts like a negative number on a number line, moving the balance left, reducing the overall asset value.

Bank Account

| Date | Details | JN | Debit (+) | Credit (-) | Balance |

|---|---|---|---|---|---|

| 01/01/20X4 | Opening Balance | 10,000.00 Dr | |||

| 01/02/20X4 | Equipment Ac | 1 | 3,000.00 Cr | 7,000.00 Dr |

Equipment Account

| Date | Details | JN | Debit (+) | Credit (-) | Balance |

|---|---|---|---|---|---|

| 01/01/20X4 | Opening Balance | 25,000.00 Dr | |||

| 01/02/20X4 | Bank Ac | 1 | 3,000.00 Dr | 28,000.00 Dr |

In this case, debits (positive movements) increase the value of the asset, and credits (negative movements) reduce it. This analogy helps explain how debits and credits maintain the balance within asset accounts—each movement either increases or decreases the value, depending on the transaction.

Liability Account

Now, let’s consider a liability account, such as a loan payable. Unlike assets, liabilities typically sit on the “negative” side of the number line because they represent obligations or amounts owed. In this context, credits increase the liability, moving the balance further left, while debits reduce it, bringing the balance closer to zero.

For example, assume the company has a loan payable with a balance of $20,000. This balance can be thought of as sitting on the negative side of the number line at -20,000. When the company makes a $5,000 repayment, this is recorded as a debit, reducing the loan balance to $15,000. On a number line, this debit is like adding a positive number, moving the liability closer to zero, from -20,000 to -15,000.

Bank Account

| Date | Details | JN | Debit (+) | Credit (-) | Balance |

|---|---|---|---|---|---|

| 01/01/20X4 | Opening Balance | 10,000.00 Dr | |||

| 15/02/20X4 | Loan Payable Ac | 2 | 5,000.00 Cr | 5,000.00 Dr |

Loan Payable Account

| Date | Details | JN | Debit (+) | Credit (-) | Balance |

|---|---|---|---|---|---|

| 01/01/20X4 | Opening Balance | 20,000.00 Cr | |||

| 15/02/20X4 | Bank Ac | 2 | 5,000.00 Dr | 15,000.00 Cr |

If the company makes another $5,000 repayment, the loan balance decreases further to $10,000, again moving the liability account to the right, closer to zero. Eventually, when the loan is fully repaid, the balance reaches zero, representing that the liability no longer exists.

This analogy helps clarify the role of debits and credits in liability accounts. Just as positive numbers move values to the right and negative numbers move them to the left on a number line, debits reduce liabilities (bringing them closer to zero), while credits increase liabilities (moving them further away from zero). The concept is essential for maintaining balance within the accounting equation and ensuring that transactions are accurately reflected in a company’s financial records.

The Historical Context: Pre-Negative Numbers in Europe

An important historical context for understanding debits and credits is that double-entry accounting was developed in Europe before the widespread acceptance of negative numbers. In the 15th century, European mathematicians were still grappling with the concept of negative numbers, which had been used in other parts of the world, such as China and India, for centuries but were not yet part of European mathematical thinking.

The double-entry system, formalized by the Italian mathematician Luca Pacioli in 1494, offered a way to represent financial losses, debts, and reductions in value without the need for negative numbers. Instead of using negatives, accountants balanced increases and decreases by using the interlocking system of debits and credits. This ensured that losses could be tracked and accounted for by recording reductions in assets or increases in liabilities, without having to represent them as negative values.

The absence of negative numbers in European mathematics at the time is one reason why debits and credits can seem counterintuitive today, especially to students familiar with modern mathematical conventions. However, once you view debits and credits as a system designed to track changes across multiple accounts, the logic of the system becomes clear.

Debits and Credits: Left and Right, Not Good and Bad

Another way to dispel confusion is to understand that, in accounting, debits and credits are simply the left and right sides of an account. The terms correspond to the structure of a ledger, where debits are recorded on the left-hand side and credits are recorded on the right-hand side. This is why the system is called “double-entry accounting”—every transaction involves at least one debit and one credit entry, ensuring that every action in the financial system is accounted for from two perspectives.

To reiterate, debits are not inherently bad, and credits are not inherently good. They are neutral terms that describe the position of an entry within the accounting system. Whether a debit increases or decreases an account depends entirely on the type of account being affected. For example, debiting an expense account increases the balance (because expenses are considered reductions in equity), while debiting a liability account decreases the balance (because it reduces the amount owed).

By viewing debits and credits as parts of a balanced, mathematical system—rather than as emotionally charged terms—students can gain a deeper and more accurate understanding of how accounting works. The system is designed to maintain balance and ensure that all financial transactions are accounted for, not to assign value judgments to those transactions.

Conclusion

Understanding debits and credits in accounting requires setting aside the common, everyday meanings of these words and embracing their role as part of an interlocking mathematical system. Rather than thinking of debits as bad and credits as good, it is more helpful to see them as tools that keep the accounting equation balanced. This system, invented in Europe before the widespread acceptance of negative numbers, provides a way to track changes in assets, liabilities, and equity without relying on negative values. Ultimately, debits and credits are the left and right sides of an account, and their primary function is to ensure the accuracy and integrity of financial records. By thinking of debits and credits in this way, students can avoid the confusion that often arises from their everyday language associations and focus on the mathematical logic that underpins the entire accounting system.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo. Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

About Us

Legal

Location

Lorem ipsum dolor sit amet, consectetur adipiscing elit.

info@accounting-training.com

123-4567-890

Copyright ©2024 Accounting Training. All Rights Reserved

Course Outline

- Concepts and Accounting

- The Three Different Natures of Accounts

- The Accounting Equation

- Accrual Accounting

- Debits and Credits

- The Journal

- Bank Reconciliation

- Adjusting Entries

- Inventory and Cost of Sales

- Depreciation

- Income Statement

- Balance Sheet

- Chart of Accounts

- Accounting Principles

- Financial Accounting

- Financial Statements

- Working Capital and Liquidity

- Cash Flow Statement

- Financial Ratios

- Accounts Receivable and Bad Debts Expense

- Accounts Payable

- Inventory and Cost of Goods Sold

- Payroll Accounting

- Bonds Payable

- Stockholders’ Equity

- Present Value of a Single Amount

- Present Value of an Ordinary Annuity

- Future Value of a Single Amount

- Nonprofit Accounting

- Break-even Point

- Improving Profits

- Evaluating Business Investments

- Manufacturing Overhead

- Nonmanufacturing Overhead

- Activity Based Costing

- Standard Costing

- About WordPress

- Log In

- Register

- Elementor Debugger

- Page Template

- Theme

- Template File: WP Page Template > Elementor - header-footer.php

- Location: Header > Added By Condition > Header

- Location: Footer > Added By Condition > Footer

- Location: Popup > Added Manually > Course Outline Menu