Comprehensive Chapter on the Balance Sheet

Introduction

The balance sheet, also referred to as the statement of financial position, is one of the key financial statements used by companies, investors, creditors, and analysts to assess a business’s financial standing at a given point in time. Unlike the income statement, which records revenues and expenses over a period, the balance sheet is a snapshot that reflects what a company owns (assets), owes (liabilities), and the value retained by owners (equity) at a single moment.

Understanding the balance sheet is critical because it provides insights into a company’s liquidity, solvency, operational efficiency, and overall financial stability. This chapter explores the structure, components, importance, and practical applications of the balance sheet.

The Accounting Equation and Balance Sheet Structure

The foundation of a balance sheet lies in the fundamental accounting equation:

Assets = Liabilities + Equity

This equation ensures that a company’s resources (assets) are funded through either obligations (liabilities) or ownership interests (equity). The balance sheet is structured into three main sections:

Assets

What the company owns

Liabilities

What the company owes

Equity

The owner's residual claim on the company

Each section is further divided into subcategories to provide a clearer understanding of financial position.

Balance Sheet Formats

Balance sheets can be presented in different formats depending on the company’s reporting preferences:

1. Account Form

The Account Form balance sheet format presents assets on the left side and liabilities and equity on the right side, mirroring the accounting equation (Assets = Liabilities + Equity). This layout resembles a T-account, where the total assets must always balance with the combined total of liabilities and shareholders’ equity. The Account Form format provides a clear, side-by-side comparison of a company’s resources and obligations, making it easier for accountants and analysts to assess financial health. However, it requires more horizontal space, which can make it less practical for published financial statements or reports with limited formatting flexibility. Although traditionally used in manual bookkeeping and early financial reporting, many modern companies prefer the Report Form balance sheet, which presents information in a vertical, column-based format for easier readability.

2. Report Form

The Report Form balance sheet format presents assets, liabilities, and equity in a vertical sequence, listing assets first, followed by liabilities, and finally shareholders’ equity at the bottom. This structure aligns with the accounting equation (Assets = Liabilities + Equity) but in a top-to-bottom format, making it more compact and easier to read in financial reports, annual statements, and regulatory filings. The Report Form is the most commonly used balance sheet format today because it allows for efficient presentation of financial data without requiring excessive horizontal space. This format is particularly useful for large corporations and publicly traded companies, where financial statements need to be clear, standardised, and easily comparable across different reporting periods.

Sample Balance Sheet (XYZ Corporation)

The heading and date of the balance sheet are crucial because they provide clarity on the financial position of the company at a specific point in time. Unlike the income statement, which covers a period, the balance sheet is a snapshot of a company’s assets, liabilities, and equity on a given date. The heading must clearly state the company’s name, the title “Balance Sheet” or “Statement of Financial Position,” and the exact date to ensure there is no confusion about what period the information reflects. This is especially important for investors, creditors, and analysts, as financial conditions can change rapidly, and outdated data could lead to incorrect assessments of a company’s financial health. A correctly dated balance sheet allows stakeholders to compare financial positions across different periods, helping in trend analysis and decision-making regarding investments, credit approvals, and strategic planning.

To illustrate the concepts discussed, below is a sample balance sheet for XYZ Corporation as of December 31, 202X.

XYZ Corporation Balance Sheet

| Assets | EUR |

|---|---|

| Current Assets | |

| Cash and Cash Equivalents | 2,500,000 Dr |

| Marketable Securities | 20,000 Dr |

| Accounts Receivable (Net) | 1,000,000 Dr |

| Inventory | 1,500,000 Dr |

| Prepaid Expenses | 50,000 Dr |

| Supplies | 40,000 Dr |

| Other Receivables | 5,000 Dr |

| Total Current Assets | 5,115,000 Dr |

| Non-Current | |

| Property, Plant & Equipment | 5,000,000 Dr |

| Intangible Assets | 2,000,000 Dr |

| Long-term Investments | 1,500,000 Dr |

| Accumulated Depreciation | 1,000,000 Cr |

| Total Non-Current Assets | 7,500,000 Dr |

| Total Assets | 12,615,000 Dr |

| Liabilities and Equity | EUR |

|---|---|

| Current Liabilities | |

| Accounts payable | 1,200,000 Cr |

| Accrued Expenses | 50,000 Cr |

| Wages payable | 200,000 Cr |

| Short-Term Bank Borrowing | 60,000 Cr |

| Current Portion of Long-Term Debt | 500,000 Cr |

| Customer Deposits (Unearned Revenue) | 100,000 Cr |

| Dividends Payable | 500,000 Cr |

| Corporation Tax Payable | 250,000 Cr |

| Fixed Asset Payable | 80,000 Cr |

| Total Current Liabilities | 2,940,000 Cr |

| Non-Current Liabilites | |

| Long-Term Debt | 4,000,000 Cr |

| Pension Fund Liabilites | 1,000,000 Cr |

| Deferred tax liabilites | 600,000 Cr |

| Provision | 50,000 Cr |

| Total Non-current Liabiliites | 5,650,000 Cr |

| Total Liabilities | 8,590,000 Cr |

| Equity | |

| Common Stock (Share Capital) | 200,000 Cr |

| Additional Paid in capital (Share premium) | 400,000 Cr |

| Retained Earnings (Retained Profit) | 3,000,000 Cr |

| Treasury Stock (Treasury Shares) | 125,000 Dr |

| Accumulated Other Comprehensive Income (Also OCI) | 550,000 Cr |

| Total Equity | 4,025,000 Cr |

| Total Liabilities and Equity | 12,615,000 Cr |

This balance sheet provides a real-world illustration of how financial data is structured and categorized.

Detailed Explanation of Balance Sheet Components

Assets (Company’s Resources)

The assets section of the balance sheet represents everything a company owns or controls that has economic value and can be used to generate future benefits. Assets are categorised based on their liquidity, meaning how quickly they can be converted into cash. Current assets, such as cash, accounts receivable, and inventory, are expected to be converted into cash or used within a year. Non-current assets, including property, plant, and equipment (PPE), as well as intangible assets like patents and trademarks, provide long-term value to the business. This distinction helps stakeholders assess a company’s ability to meet short-term obligations and its investment in long-term growth. Assets are usually recorded at historical cost, meaning their original purchase price, though some assets, such as marketable securities, may be adjusted to fair market value.

From a broader financial perspective, the assets section of the balance sheet reveals how efficiently a company allocates and utilises resources. A company with a strong base of productive assets, such as well-maintained machinery or valuable intellectual property, is generally better positioned for sustained profitability. Investors and analysts examine asset composition to gauge financial health, stability, and future earning potential. For instance, a company with excessive current assets relative to liabilities may indicate strong liquidity, whereas an overreliance on non-current assets could suggest higher capital investment but lower short-term flexibility. By studying this section, businesses can optimise asset management strategies, ensuring they maintain the right balance between liquidity, operational efficiency, and long-term value creation.

Current Assets

Current assets are the short-term resources a company owns that are expected to be converted into cash, sold, or consumed within a financial year or the business’s operating cycle, whichever is longer. They are essential for maintaining daily operations and meeting short-term financial obligations. Typical current assets include cash and cash equivalents, which provide immediate liquidity; accounts receivable, representing money owed by customers for goods or services provided on credit; inventory, which consists of products held for sale; and prepaid expenses, such as rent or insurance paid in advance. Current assets are crucial indicators of a company’s liquidity and financial flexibility, helping investors and analysts determine whether the business has enough readily available resources to cover its short-term liabilities. A healthy balance of current assets ensures that a company can smoothly manage its operational expenses while maintaining financial stability.

Cash and Cash Equivalents: are the most liquid assets listed under current assets on a balance sheet, representing money that is immediately available for use. This category includes physical cash, bank balances, and short-term investments that can be quickly converted into cash, such as treasury bills and money market funds. These assets are vital for a company’s liquidity, ensuring it can meet immediate financial obligations, such as paying suppliers, covering wages, and handling unexpected expenses. Since cash and cash equivalents have no significant risk of losing value, they provide businesses with the flexibility needed to operate smoothly and respond to financial needs without delay.

Marketable Securities: are short-term investments classified under current assets on a balance sheet because they can be easily converted into cash within a short period, typically less than a year. These securities include stocks, bonds, treasury bills, and commercial paper, all of which are highly liquid and traded in active markets. Companies invest in marketable securities to earn a return on excess cash while maintaining financial flexibility. Unlike cash, these assets may fluctuate in value, but they remain a low-risk investment that can be quickly sold to generate funds for operational needs or unexpected expenses.

Accounts Receivable (Net): represents the amount a company is owed by customers for goods or services sold on credit, after deducting an allowance for doubtful accounts (expected non-payments). It is listed under current assets on the balance sheet, as it is expected to be collected within the normal operating cycle, usually within 30 to 90 days. A high accounts receivable balance indicates strong sales, but excessive outstanding receivables may suggest collection issues or customer payment delays. By monitoring accounts receivable (net), businesses can assess their cash flow efficiency and ensure they maintain healthy liquidity while minimising the risk of bad debts.

Inventory refers to the goods a company holds for sale or production and is classified as a current asset on the balance sheet because it is expected to be sold or used within the business’s operating cycle. It includes raw materials, work-in-progress, and finished goods, depending on the type of business. Inventory is valued using methods such as FIFO (First-In, First-Out), LIFO (Last-In, First-Out), or weighted average cost, which impact financial statements differently. Managing inventory efficiently is crucial for maintaining cash flow and profitability, as excessive stock ties up capital, while insufficient inventory can lead to lost sales. Monitoring inventory levels helps businesses strike the right balance between meeting customer demand and controlling storage and procurement costs.

Prepaid Expenses: are advance payments made by a company for goods or services that will be received or used in the future, and they are recorded as current assets on the balance sheet rather than as expenses. This is because, at the time of payment, the company has not yet received the full benefit of the service, meaning the amount paid represents a right to future economic benefits rather than an incurred cost. Common prepaid expenses include insurance premiums, rent, subscriptions, and maintenance contracts. As the service is provided or time passes, the prepaid amount is gradually expensed on the income statement. This ensures accurate financial reporting by matching expenses to the periods in which they are actually incurred, rather than when they were paid.

Supplies are tangible items that a company purchases for use in daily operations but that are not intended for resale, and they are recorded as a current asset on the balance sheet until they are used. Unlike inventory, which consists of goods meant for sale, supplies include items such as office materials, packaging materials, and maintenance tools that support business activities. Supplies are initially classified as an asset because they represent a future economic benefit, but as they are consumed, their cost is gradually expensed on the income statement. Proper management of supplies ensures that a company maintains adequate resources for operations while avoiding unnecessary stockpiling that could lead to waste or inefficiencies.

Other receivables refer to amounts owed to a company that do not fall under accounts receivable and are classified as a current asset on the balance sheet if they are expected to be collected within a year. These can include tax refunds, employee advances, insurance claims, interest receivable, or loans given to third parties. While similar to accounts receivable, which arise from sales on credit, other receivables originate from non-trading transactions. Managing other receivables effectively is important for maintaining cash flow and liquidity, ensuring that the company recovers outstanding amounts in a timely manner. If these receivables become doubtful or uncollectible, they may need to be written off as bad debts.

Non-Current Assets

Non-current assets are long-term resources that a company owns and controls and are not expected to be converted into cash within the next financial year or operating cycle. They are essential for a business’s ongoing operations and future growth, representing investments in infrastructure, technology, and intellectual property. These assets include property, plant, and equipment (PPE), intangible assets such as patents and trademarks, long-term investments, and deferred tax assets. Unlike current assets, which are used or sold within a short timeframe, non-current assets provide long-term value and stability, often forming the foundation of a company’s ability to generate revenue. They are usually recorded at historical cost, with some assets being subject to depreciation, amortisation, or impairment over time to reflect their declining value or usefulness.

From a balance sheet perspective, non-current assets play a crucial role in a company’s financial health and strategic positioning. A business with significant non-current assets may be capital-intensive, meaning it has invested heavily in fixed resources to support its operations. While these assets do not directly contribute to liquidity, they are often essential for securing long-term financing and investment, as they can be used as collateral for loans. Investors and analysts examine the composition, condition, and valuation of non-current assets to assess the sustainability of a company’s business model. However, because non-current assets are often subject to accounting estimates and subjective valuation methods, they may not always reflect their true market value, making it important to consider them alongside other financial indicators when analysing a balance sheet.

Property, Plant & Equipment (PPE) refers to tangible, long-term assets that a company owns and uses in its operations to generate revenue. It includes land, buildings, machinery, vehicles, and equipment, all of which are essential for sustaining business activities. PPE is classified as a non-current asset on the balance sheet because it is not expected to be converted into cash within a year. Over time, most PPE assets depreciate, meaning their value is gradually reduced to reflect wear and tear or obsolescence, except for land, which is typically not depreciated. The net book value of PPE is recorded as cost minus accumulated depreciation, giving stakeholders insight into the company’s investment in infrastructure and operational capacity. The amount and condition of PPE on the balance sheet help investors and analysts assess a company’s capital expenditure, efficiency, and long-term financial stability.

Intangible assets are non-physical, long-term assets that provide a company with economic value and competitive advantage, and they are recorded under non-current assets on the balance sheet. These assets include patents, trademarks, copyrights, goodwill, brand recognition, and proprietary technology, all of which contribute to a business’s future revenue generation. Unlike tangible assets such as machinery or buildings, intangible assets do not have a physical presence but can still be valuable corporate resources. Many intangible assets are amortised over their useful life to reflect their gradual consumption, except for those with indefinite life spans, such as goodwill, which must be tested for impairment regularly. The presence of intangible assets on the balance sheet indicates a company’s intellectual property, brand strength, and innovation potential, making them critical for industries like technology, pharmaceuticals, and media.

Long-term investments are financial assets that a company holds for an extended period, typically beyond one year, and are recorded under non-current assets on the balance sheet. These investments can include stocks, bonds, real estate, joint ventures, and ownership stakes in other companies, often acquired to generate income, capital appreciation, or strategic business advantages rather than for immediate resale. Unlike current investments, which are liquid and intended for short-term gains, long-term investments reflect a company’s commitment to future growth and financial stability. Depending on their nature, these assets may be accounted for using cost, fair value, or equity method accounting, ensuring they accurately represent their market worth or ownership influence. The presence of long-term investments on a balance sheet can indicate a financially strong company with a diversified asset base, lower risk exposure, and a strategy focused on sustained profitability and expansion.

Accumulated depreciation is a contra-asset account that reflects the total amount of depreciation expense recorded against non-current assets over time, reducing their book value on the balance sheet. It applies to tangible assets such as buildings, machinery, equipment, and vehicles, but not to land, as land is generally considered to have an indefinite useful life. Since accumulated depreciation offsets the original cost of depreciable assets, it does not appear as a liability but instead reduces the reported value of Property, Plant & Equipment (PPE). This helps provide a more realistic valuation of an asset’s remaining useful life and economic benefit to the company. The balance of accumulated depreciation increases each year as depreciation expenses are recorded, and when an asset is fully depreciated or disposed of, its accumulated depreciation is removed from the balance sheet. Understanding accumulated depreciation is essential for analysing a company’s capital efficiency, asset management, and long-term investment strategy, as it directly impacts the valuation of non-current assets and financial decision-making.

Liabilities (Company’s Obligations)

Liabilities represent a company’s financial obligations or debts that it is legally required to settle in the future. They are classified on the balance sheet based on their due dates, with current liabilities being those payable within a year and non-current liabilities being long-term obligations extending beyond a year. Liabilities arise from a variety of business activities, including borrowing funds, purchasing goods or services on credit, accruing expenses, or fulfilling contractual obligations. They are an essential component of the accounting equation (Assets = Liabilities + Equity) and play a key role in determining a company’s financial health. A company’s ability to manage its liabilities efficiently is crucial, as excessive debt can increase financial risk, whereas well-structured liabilities can support growth and investment opportunities.

On the balance sheet, current liabilities typically include accounts payable, interest payable, wages payable, short-term loans, and unearned revenue, reflecting the company’s immediate financial obligations. Non-current liabilities, such as long-term loans, bonds payable, deferred tax liabilities, and pension obligations, indicate more structured, long-term financial commitments. While liabilities represent amounts owed, they are not inherently negative; many businesses rely on liabilities to finance expansion, acquire assets, or manage cash flow effectively. Investors and analysts examine a company’s liabilities in relation to its assets and equity to assess financial leverage and solvency, using key ratios such as the debt-to-equity ratio and current ratio. Proper management of liabilities ensures that a company can meet its obligations without jeopardising liquidity or long-term financial stability.

Current Liabilities

Current liabilities are short-term financial obligations that a company must settle within a year or its operating cycle, whichever is longer, and they are listed under liabilities on the balance sheet. They typically include accounts payable, short-term loans, interest payable, wages payable, accrued expenses, and unearned revenue. Current liabilities are crucial indicators of a company’s short-term financial health and liquidity, as they highlight the immediate demands on its cash and other current assets. A business must ensure it has sufficient current assets to cover its current liabilities, and financial analysts often use the current ratio (current assets ÷ current liabilities) to assess whether a company can meet its short-term obligations without financial strain. Managing current liabilities effectively is essential to maintaining operational stability and financial flexibility.

Accounts payable refers to amounts a company owes to suppliers for goods for resale or raw materials purchased on credit and is recorded as a current liability on the balance sheet. It represents short-term trade obligations that must be settled within the agreed payment terms, usually within 30 to 90 days. Unlike accrued expenses, which cover obligations for services received (such as wages or utilities), accounts payable specifically relates to inventory purchases and direct production materials. Managing accounts payable efficiently is crucial for maintaining good supplier relationships and cash flow, as delayed payments can affect credit terms and supplier trust. A company’s accounts payable turnover ratio helps assess how efficiently it pays suppliers and manages working capital.

Accrued expenses are obligations a company has incurred for services received but not yet paid for, and they are recorded as a current liability on the balance sheet. It is important to note that accrued expenses are not expenses themselves, but rather a measurement of outstanding liabilities owed to entities that have already provided a service. These can include utilities, professional fees, rent, interest on loans, and maintenance costs, where the service has been used but the invoice has not yet been settled. Accrued expenses ensure that a company’s financial statements accurately reflect obligations in the correct accounting period, following the accrual principle. Proper management of accrued expenses is essential for maintaining transparent financial reporting and a clear understanding of short-term financial commitments.

Wages payable is a current liability on the balance sheet that represents amounts owed to employees for work already performed but not yet paid. This liability often arises because payroll is typically processed after the end of a work period, meaning wages earned in one accounting period may not be paid until the next. It is important to note that wages payable can often be split into two components: the net wages owed to employees and the amounts withheld for taxes, such as income tax, national insurance, or pension contributions, which must be remitted to the government. Managing wages payable efficiently is crucial for maintaining employee trust and ensuring compliance with tax regulations, as delayed payments to employees or tax authorities can result in financial penalties and reputational damage.

Short-term bank borrowing is a current liability on the balance sheet that represents loans or credit facilities a company has drawn from a bank that are due for repayment within one year. These borrowings are often used to cover short-term cash flow needs, finance working capital, or manage seasonal fluctuations in revenue. They can take the form of overdrafts, revolving credit facilities, or short-term loans, usually carrying interest costs that must be accounted for separately under accrued interest. Effective management of short-term bank borrowing is essential to ensure a company maintains adequate liquidity without becoming overly reliant on debt, as excessive short-term borrowing can signal financial strain and impact a company’s creditworthiness.

Current portion of long-term debt is a current liability on the balance sheet that represents the portion of a company’s long-term debt that is due for repayment within the next 12 months. This includes scheduled repayments on bank loans, bonds, mortgages, or other long-term borrowing arrangements. Unlike short-term bank borrowing, which is typically used for working capital needs, the current portion of long-term debt is a planned repayment of existing long-term financial obligations. Companies must ensure they have sufficient liquidity to meet these repayments, as failure to do so could result in penalties, credit rating downgrades, or financial distress. Analysts and investors closely monitor this liability to assess whether a company has the financial strength to meet its short-term debt commitments without jeopardising long-term stability.

Other receivables refer to amounts owed to a company that do not fall under accounts receivable and are classified as a current asset on the balance sheet if they are expected to be collected within a year. These can include tax refunds, employee advances, insurance claims, interest receivable, or loans given to third parties. While similar to accounts receivable, which arise from sales on credit, other receivables originate from non-trading transactions. Managing other receivables effectively is important for maintaining cash flow and liquidity, ensuring that the company recovers outstanding amounts in a timely manner. If these receivables become doubtful or uncollectible, they may need to be written off as bad debts.

Customer deposits (unearned revenue) is a current liability on the balance sheet that represents payments received from customers for goods or services that have not yet been delivered or fulfilled. This liability arises when a company collects money in advance, such as prepayments for subscriptions, deposits for custom orders, or advance payments for services. Until the company provides the promised goods or services, the amount remains a liability, as the business has an obligation to either deliver or refund the payment. Once the product or service is provided, the liability is reduced, and the revenue is recognised on the income statement. Managing unearned revenue properly is essential for ensuring accurate financial reporting, maintaining customer trust, and aligning revenue recognition with performance obligations.

Dividends payable is a current liability on the balance sheet that represents declared but unpaid dividends owed to shareholders. This liability arises when a company’s board of directors approves and announces a dividend payment, but the actual distribution has not yet occurred. Once declared, the company has a legal obligation to pay the dividend, and it remains a liability until the payment is made to shareholders. Dividends payable typically appear for a short period between the declaration date and the payment date, after which the liability is settled. Proper management of this liability ensures timely payments to investors, maintains shareholder confidence, and reflects the company’s commitment to returning value to its owners.

Corporation tax payable is a current liability on the balance sheet that represents the amount of corporation tax owed to the government based on the company’s taxable profits but not yet paid. This liability arises because businesses typically calculate and report their tax obligations periodically, often on a quarterly or annual basis, but payment is made at a later date. The amount recorded under corporation tax payable reflects the outstanding tax liability that must be settled in the near term. Proper management of this liability is crucial to ensure compliance with tax regulations, avoid penalties or interest charges, and maintain a strong financial position. Since tax laws can be complex and vary by jurisdiction, companies must carefully plan for their tax obligations to ensure they have sufficient liquidity to meet payment deadlines

Fixed asset payable is a current liability on the balance sheet that represents the amount owed for the purchase of a fixed asset that has been acquired but not yet paid for. While it is not commonly seen on most balance sheets, it can appear when a company purchases property, plant, or equipment (PPE) on credit instead of paying immediately. Typically, companies finance fixed asset purchases through long-term loans or leasing arrangements, making this liability less frequent compared to standard accounts payable, which is used for operational expenses. However, when a supplier allows deferred payment terms for a capital asset, fixed asset payable is recorded as a short-term obligation until settlement. Although rare, its presence on the balance sheet indicates that a company has chosen to delay payment on a capital investment, requiring careful cash flow management to ensure timely repayment without straining liquidity.

Non-Current Liabilities

The long-term liabilities section of the balance sheet represents a company’s financial obligations that are not due within the next 12 months. These liabilities are crucial for funding major investments, infrastructure, and long-term business growth. Unlike current liabilities, which require immediate payment, long-term liabilities allow companies to spread out their financial obligations over several years, reducing short-term financial pressure. This section typically includes long-term debt, bonds payable, lease obligations, pension liabilities, and deferred tax liabilities, all of which reflect commitments that extend beyond a single financial period. By securing long-term financing, businesses can invest in expansion, acquire new assets, or fund strategic projects without straining their immediate liquidity. However, managing these liabilities effectively is essential, as excessive long-term debt can increase financial risk and interest costs, potentially affecting profitability and creditworthiness.

From an analytical perspective, long-term liabilities are a key indicator of a company’s capital structure and financial health. Investors and creditors closely examine the debt-to-equity ratio to assess whether a company is over-leveraged or maintaining a sustainable level of debt. A well-balanced capital structure, where long-term liabilities are matched with strong assets and revenue-generating capabilities, can support business growth without exposing the company to undue financial stress. Additionally, some long-term liabilities, such as pension obligations and deferred tax liabilities, arise from regulatory or accounting requirements, reflecting future obligations rather than borrowed funds. Understanding the composition of long-term liabilities helps stakeholders determine the company’s ability to meet its financial commitments over time, ensuring that it remains solvent and positioned for long-term success.

Long-term debt is a non-current liability on the balance sheet that represents borrowed funds that are due for repayment beyond 12 months. This can include bank loans, corporate bonds, mortgages, and other forms of debt financing that companies use to fund large capital expenditures, expansion projects, or strategic acquisitions. Unlike short-term debt, which must be repaid within a year, long-term debt allows businesses to spread out repayments over an extended period, making it a crucial part of a company’s capital structure. While taking on long-term debt can provide necessary funding for growth, it also introduces financial risk, as companies must ensure they generate enough revenue to cover interest payments and principal repayments. Analysts and investors closely examine a company’s debt-to-equity ratio and interest coverage ratio to assess whether its long-term debt levels are sustainable. Proper management of long-term debt ensures a company can benefit from financial leverage while maintaining solvency and financial stability over time.

Pension fund liabilities are a non-current liability on the balance sheet that represent a company’s obligation to pay retirement benefits to its employees in the future. These liabilities arise when a company offers defined benefit pension plans, where it guarantees employees a specific payout upon retirement based on factors such as salary and years of service. Unlike defined contribution plans, where the company’s obligation is limited to contributions made, pension fund liabilities can grow significantly if the company’s pension plan is underfunded—meaning that the assets set aside to cover future payouts are insufficient. These liabilities are highly sensitive to interest rates, investment returns, and actuarial assumptions, making them a key focus for analysts assessing a company’s long-term financial health. Managing pension fund liabilities effectively is crucial to ensuring that a business meets its obligations to retirees without placing excessive strain on future cash flows and profitability.

Deferred tax liabilities are a non-current liability on the balance sheet that represent tax obligations a company will need to pay in the future due to temporary differences between accounting income and taxable income. These differences arise when certain revenues or expenses are recognised at different times for financial reporting and tax purposes, often due to depreciation methods, revenue recognition rules, or tax incentives. For example, if a company uses accelerated depreciation for tax purposes but straight-line depreciation for accounting purposes, it will initially report lower taxable income than accounting income, creating a deferred tax liability that must be settled in later years. While deferred tax liabilities do not require immediate payment, they indicate that the company will face higher tax expenses in the future, making it important for businesses to plan accordingly. Analysts and investors monitor deferred tax liabilities to assess their potential impact on future cash flows and overall financial stability.

A provision is a liability recognised on the balance sheet when a company has a present obligation due to a past event, and it is probable that a future cash outflow will be required to settle it. This differs from contingent liabilities, which are not recorded on the balance sheet because they are uncertain. Provisions commonly arise from legal disputes, warranties, environmental obligations, or restructuring costs, where the company has a clear obligation but the exact amount or timing of the payment may be uncertain. Since provisions represent expected future cash outflows, they reduce a company’s net assets and equity, impacting its overall financial position. Proper recognition of provisions ensures that the balance sheet accurately reflects the company’s obligations and financial risks, preventing misrepresentation of available financial resources.

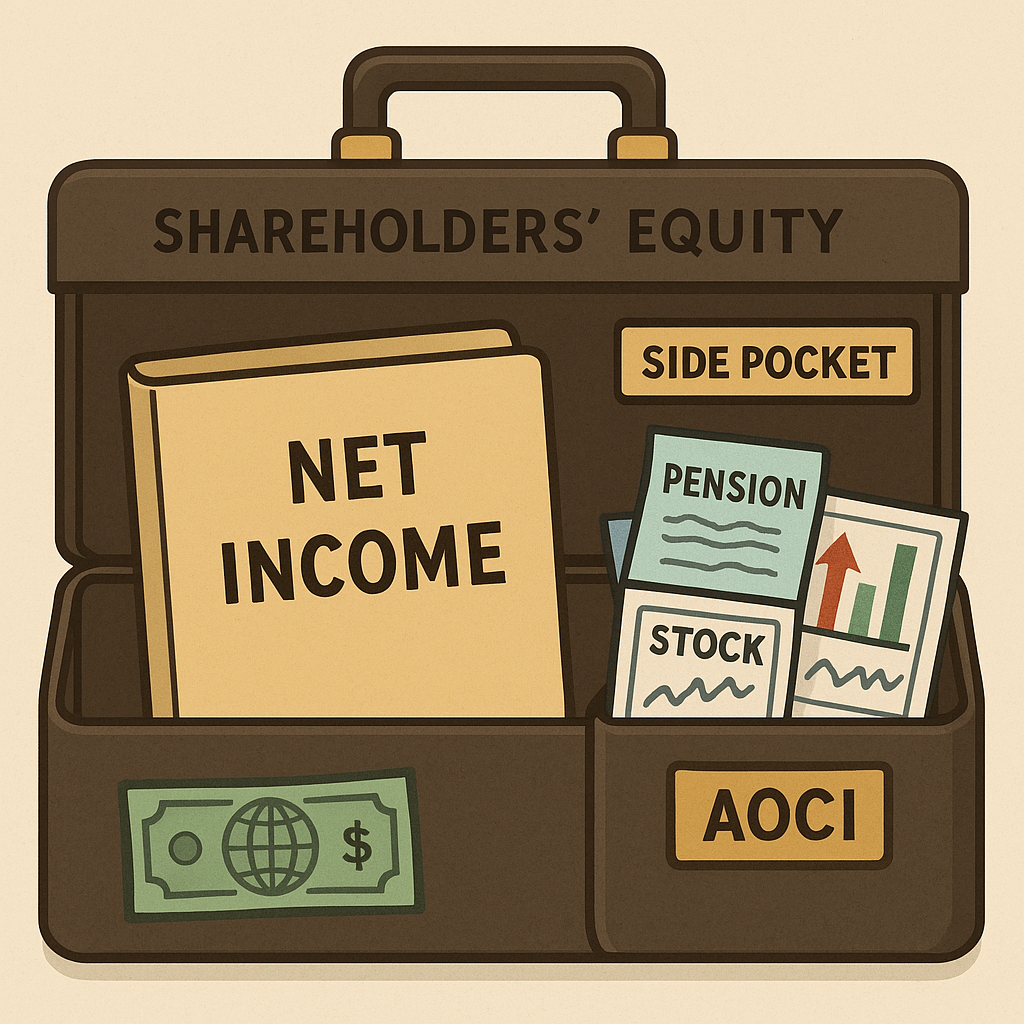

Shareholders' Equity

The equity section of the balance sheet represents the ownership interest in a company after deducting all liabilities from its assets. It reflects the net worth of the business and consists of several key accounts, including share capital (common stock), share premium (additional paid-in capital), retained earnings, treasury shares, and reserves. Share capital (common stock) represents the funds raised through issuing shares, while share premium (additional paid-in capital) reflects the excess amount received over the nominal or par value of shares issued. Retained earnings consist of accumulated profits that have been reinvested into the company rather than distributed as dividends. The equity section may also include other reserves, such as the revaluation reserve and other comprehensive income (OCI), also known as accumulated other comprehensive income (AOCI) in the U.S., which captures unrealized gains or losses that do not pass through the income statement. The equity section is a key indicator of financial stability, showing how much of a company’s assets are financed by shareholders rather than creditors, making it essential for assessing long-term financial health.

Equity is closely tied to the accounting equation (Assets = Liabilities + Equity), ensuring the balance sheet remains balanced. It is also a critical metric for investors evaluating a company’s profitability and capital structure, particularly through ratios such as return on equity (ROE), which measures how effectively a company generates profits from shareholder investments. A strong equity position generally indicates a financially stable company with the ability to fund growth without excessive reliance on debt. However, equity can fluctuate due to factors such as dividend payments, share buybacks (treasury stock), or accumulated losses, all of which impact shareholders’ residual claims. The inclusion of share premium (additional paid-in capital) and other comprehensive income (AOCI/OCI) provides further insight into how a company manages its financial resources and capital inflows. Ultimately, the equity section is a fundamental component of the balance sheet, offering valuable insights into a company’s financial strength, growth potential, and long-term sustainability.

The common stock account, also known as the share capital account, represents the par value of shares that a company has issued to investors and is recorded under equity on the balance sheet. It reflects the initial capital investment provided by shareholders in exchange for ownership in the company. However, since many shares are issued at a price above their par value, the excess amount is recorded separately in the share premium account (additional paid-in capital in the U.S.). While the common stock account itself does not fluctuate frequently, it may increase when a company issues new shares or decrease in rare cases where shares are retired or cancelled. This account is a fundamental part of the equity section, as it indicates the company’s funding through share issuance and forms the base of shareholder ownership, distinguishing it from retained earnings and other reserves.

The additional paid-in capital (APIC) account, known as the share premium account in the UK, represents the amount investors have paid for shares above their nominal or par value and is recorded under equity on the balance sheet. When a company issues shares at a price higher than their stated par value, the excess amount is credited to this account, reflecting the extra capital contributed by shareholders beyond the basic share capital. Unlike retained earnings, which come from profits, APIC/share premium arises solely from share issuance activities and does not fluctuate unless the company issues new shares or engages in certain equity transactions, such as share buybacks. This account plays an important role in strengthening a company’s financial position, as it represents additional funds raised that can be used for business expansion, acquisitions, or other corporate activities, without increasing liabilities or taking on debt.

The retained earnings account, known as retained profit in the UK, represents the accumulated net income that a company has reinvested in the business rather than distributed to shareholders as dividends. It is recorded under equity on the balance sheet and grows when a company earns a profit and retains it for future use. Retained earnings can be used for expansion, research and development, paying down debt, or funding acquisitions, making it a crucial indicator of a company’s ability to self-finance its growth. However, if a company incurs losses, retained earnings decrease, and in cases of prolonged negative balances, it may be referred to as accumulated deficit. Unlike share capital or additional paid-in capital, retained earnings fluctuate based on a company’s profitability and dividend policies, reflecting the company’s long-term financial health and reinvestment strategy.

Accumulated Other Comprehensive Income (AOCI), also known as Other Comprehensive Income (OCI) under International Financial Reporting Standards (IFRS), represents unrealised gains and losses that have not yet been recognised in net income and are instead recorded directly in equity. These can include items such as foreign currency translation adjustments, unrealised gains or losses on available-for-sale financial assets, pension adjustments, and changes in the fair value of certain derivatives. AOCI is presented as a separate component of shareholders’ equity on the balance sheet, as these gains and losses may never be realised or may impact financial results in future periods. Unlike retained earnings, which reflect past profits available for reinvestment, AOCI captures temporary changes in asset and liability values that are not included in net income until they are realised. Investors and analysts monitor AOCI to gain insight into a company’s financial exposure to foreign exchange, interest rates, and market fluctuations, as it can impact future profitability and overall equity value.

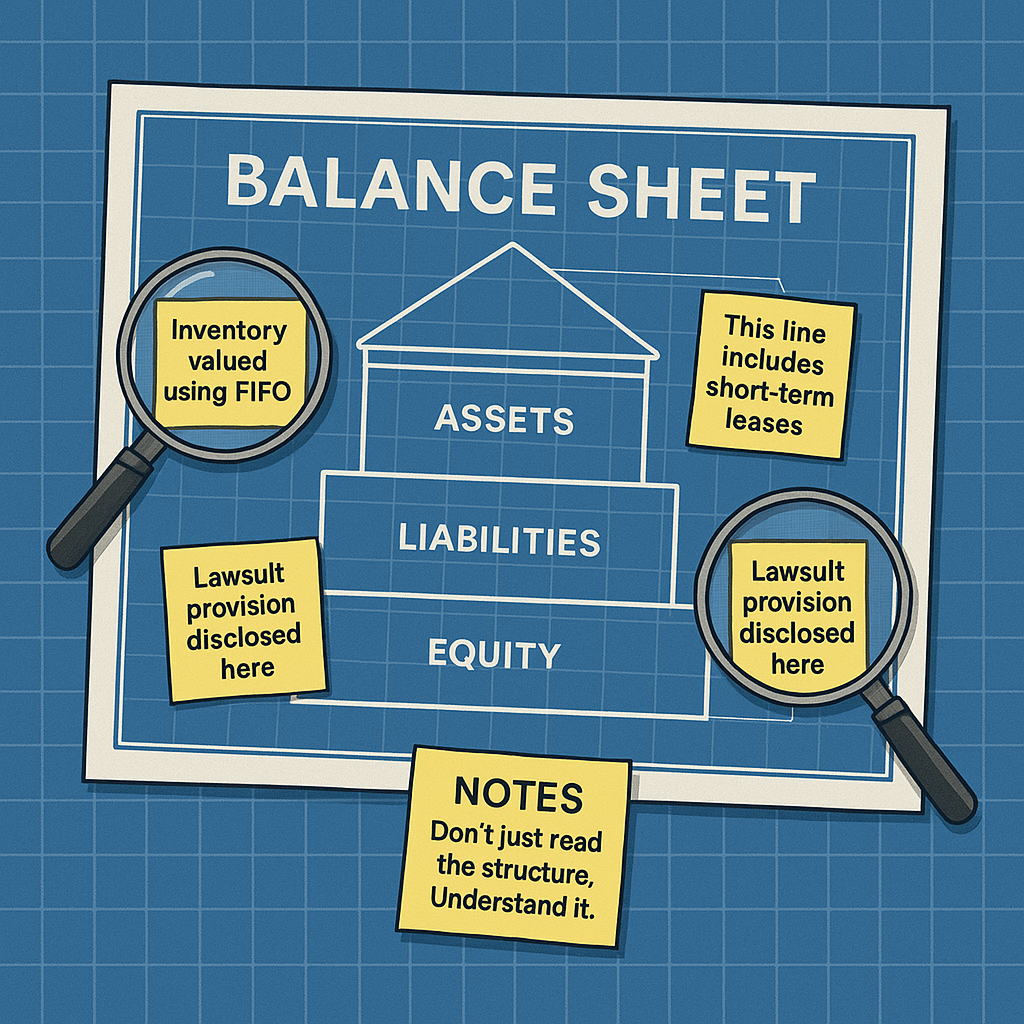

Notes to the Financial Statements

The notes to the financial statements are an essential companion to the balance sheet, providing the context, detail, and explanations necessary to fully understand the figures presented. While the balance sheet gives a snapshot of a company’s financial position at a specific point in time, the notes elaborate on the accounting policies used, explain individual line items, and disclose judgements, estimates, and risks that cannot be captured in the face of the statement alone. For example, notes may provide a breakdown of property, plant and equipment, outline the terms of long-term debt, or clarify the nature of provisions and contingent liabilities. Without the notes, stakeholders would lack vital information needed to interpret the balance sheet with confidence and accuracy.

Under both IFRS and US GAAP, the notes serve a similar purpose, but there are differences in emphasis and disclosure requirements. IFRS, for example, often places a stronger focus on principles-based disclosures, requiring entities to explain the reasoning behind significant accounting decisions and assumptions. US GAAP, being more rules-based, tends to have more prescriptive and detailed disclosure requirements for certain areas, such as leases, pension obligations, and fair value measurements. Regardless of the framework, both standards require companies to include disclosures that reflect the nature, timing, and uncertainty of assets, liabilities, and equity positions. This allows users of the financial statements to better assess a company’s financial health, risks, and performance.

Importantly, the notes also include disclosures on items that may not appear directly on the balance sheet, such as contingent liabilities, commitments, and events after the reporting period. These disclosures help users evaluate potential impacts on the company’s future financial position. Additionally, they often explain how values were determined—such as valuation methods for investments or impairment testing for assets—which is crucial for assessing the reliability of the balance sheet figures. In essence, the notes are integral to the balance sheet’s usefulness, providing the transparency and depth needed for informed financial decision-making by investors, creditors, regulators, and other stakeholders.

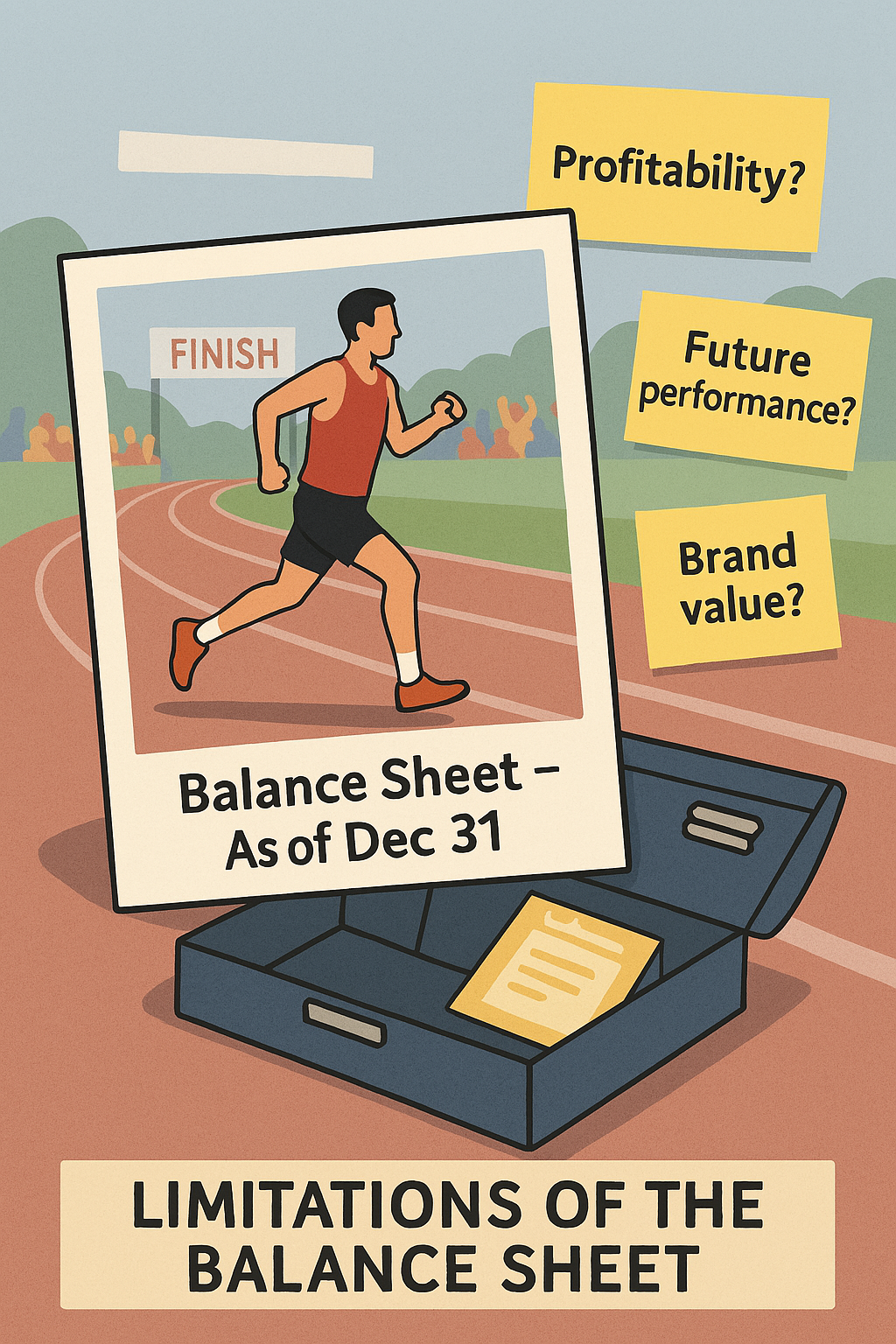

Limitations of the Balance Sheet

While the balance sheet is a vital tool for assessing a company’s financial position, it has several limitations that must be acknowledged when interpreting its figures. One of the primary limitations is that it represents a snapshot at a single point in time, meaning it does not capture changes in financial position before or after the reporting date. As a result, users of financial statements may miss significant movements in a company’s financial health that occur shortly after the balance sheet date. Furthermore, the balance sheet often records assets and liabilities at historical cost, rather than fair market value, which may not reflect their current economic worth. This can be particularly misleading during times of inflation or market volatility, where real asset values may differ significantly from those recorded.

Another key limitation lies in the fact that the balance sheet does not capture all valuable aspects of a business, particularly internally generated intangible assets such as brand reputation, employee expertise, customer loyalty, and intellectual property, unless these have been acquired in a transaction. These elements can be significant drivers of value, especially in knowledge-based industries, yet they are not reflected on the balance sheet. Additionally, many items involve judgements and estimates—such as provisions, depreciation, and impairment—which can vary widely between companies and reduce comparability. For a full understanding of a company’s financial position and performance, the balance sheet should be analysed alongside the income statement, cash flow statement, and the notes to the financial statements, which provide crucial context, detail, and disclosures about assumptions and risks.

Importance of the Balance Sheet

The balance sheet is one of the most important financial statements because it provides a clear and structured snapshot of a company’s financial position at a specific point in time. It shows what the business owns (assets), owes (liabilities), and the residual interest belonging to shareholders (equity), giving a concise picture of the company’s financial health. This information is crucial for a wide range of stakeholders, including investors, lenders, management, and regulators, who rely on it to assess the organisation’s liquidity, solvency, and capital structure. For example, by comparing current assets to current liabilities, one can gauge the company’s ability to meet its short-term obligations, while the overall balance of equity and debt highlights its reliance on external financing versus shareholder funding.

Beyond the basic figures, the balance sheet helps in strategic decision-making and financial analysis. Investors use it to determine whether a company is financially stable and capable of delivering long-term returns, while creditors assess whether it can repay loans and other obligations. Internally, management relies on the balance sheet to track resource allocation, evaluate financial performance, and plan for growth or restructuring. It also forms the foundation for key financial ratios, such as the current ratio, debt-to-equity ratio, and return on equity, which provide deeper insights into operational and financial efficiency. While the balance sheet alone does not tell the full story of a business, it is a fundamental tool for understanding financial standing and supporting informed, responsible decision-making.

Conclusion

The balance sheet is a powerful tool for understanding a company’s financial position. By studying its components, financial professionals can assess liquidity, solvency, and profitability. However, it should always be analysed alongside other financial statements for a comprehensive view of a company’s financial health.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo. Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

About Us

Legal

Location

Lorem ipsum dolor sit amet, consectetur adipiscing elit.

info@accounting-training.com

123-4567-890

Copyright ©2024 Accounting Training. All Rights Reserved

Course Outline

- Concepts and Accounting

- The Three Different Natures of Accounts

- The Accounting Equation

- Accrual Accounting

- Debits and Credits

- The Journal

- Bank Reconciliation

- Adjusting Entries

- Inventory and Cost of Sales

- Depreciation

- Income Statement

- Balance Sheet

- Chart of Accounts

- Accounting Principles

- Financial Accounting

- Financial Statements

- Working Capital and Liquidity

- Cash Flow Statement

- Financial Ratios

- Accounts Receivable and Bad Debts Expense

- Accounts Payable

- Inventory and Cost of Goods Sold

- Payroll Accounting

- Bonds Payable

- Stockholders’ Equity

- Present Value of a Single Amount

- Present Value of an Ordinary Annuity

- Future Value of a Single Amount

- Nonprofit Accounting

- Break-even Point

- Improving Profits

- Evaluating Business Investments

- Manufacturing Overhead

- Nonmanufacturing Overhead

- Activity Based Costing

- Standard Costing

- About WordPress

- Log In

- Register

- Elementor Debugger

- Page Template

- Theme

- Template File: WP Page Template > Elementor - header-footer.php

- Location: Header > Added By Condition > Header

- Location: Footer > Added By Condition > Footer

- Location: Popup > Added Manually > Course Outline Menu